Digital transformation in banking is often described as a technology programme. In practice, it is much bigger than that. It changes how banks serve customers, manage risks, respond to regulations, and launch new products.

For banking leaders, the challenge is not simply to digitize legacy processes. It is to redesign the organization around speed, visibility, and better decisions, while keeping customer trust and regulatory accountability intact.

The banks making the strongest progress are treating transformation as a business shift powered by data, intelligence, and modern operating models, not as a standalone IT upgrade.

If you are responsible for banking strategy, operations, risk, compliance, data, or customer experience, this article will help you understand what transformation looks like today and where to focus next.

Why Digital Transformation Matters Now?

Several forces are converging to make transformation unavoidable.

Regulators Are Rewriting the Rules

In the UK and Europe, regulation is shaping transformation priorities as strongly as customer demand and competition.

PSD2 and open banking accelerated API-based connectivity and gave regulated third parties access to customer-permissioned financial data and payment initiation in specific scenarios. In the UK, open banking has continued to expand, with millions of users now relying on open-banking-enabled services.

The FCA’s Consumer Duty has also raised the bar for monitoring and evidencing customer outcomes. Recent FCA reviews have emphasised that firms need stronger outcomes monitoring, clearer metrics, and better evidence that issues are being identified and addressed.

For many banks, regulation is no longer just a compliance obligation. It is a design constraint that influences data strategy, governance, reporting, and customer journeys.

Customers Expect Real-Time Everything

The gap between what customers expect and what traditional banks deliver is widening.

Customers now want:

- Instant account opening

- Real-time payments

- Personalised financial advice

- Seamless experiences across mobile, web, and branch

Customers increasingly compare their bank with the best digital experiences they have anywhere else. They expect fast onboarding, timely updates, consistent service across channels, and less friction when resolving problems or making decisions.

When those basics are missing, digital-first competitors become harder to ignore.

Fintechs Are Raising the Bar

Neobanks like Monzo, Revolut, and Starling have redefined customer expectations.

They offer:

- Instant onboarding

- Real-time notifications

- Intuitive user experiences

- Lower fees

Challenger banks and fintechs have shown what streamlined onboarding, intuitive interfaces, and faster product delivery can look like. Their success has pushed incumbent banks to simplify journeys, modernise infrastructure, and shorten delivery cycles.

For established institutions, the question is not whether they can innovate, but how quickly they can modernise without adding unnecessary operational and regulatory risk.

Margins Are Under Pressure

Operating costs remain high for traditional banks due to:

- Legacy IT systems requiring constant maintenance

- Manual processes in risk, compliance, and operations

- Regulatory overhead

Digital transformation offers a way to reduce costs while improving customer experience and compliance, if done strategically.

Where Banks Are Focusing Transformation Efforts

Digital transformation in banking typically centres on four interconnected areas.

| Transformation Area | What It Involves | Business Outcome |

| Customer Experience | Omnichannel banking, personalisation, self-service, real-time engagement | Improved satisfaction, retention, and lifetime value |

| Risk & Compliance | Real-time fraud detection, AML monitoring, regulatory reporting, explainable AI | Reduced fraud loss, regulatory confidence, faster compliance |

| Core Banking Modernisation | Moving from monolithic systems to cloud-native, API-enabled platforms | Faster product launches, lower costs, greater agility |

| Data & AI Foundation | Unified data platforms, real-time analytics, AI-driven decisions | Better decision-making, scalable AI, cross-functional insights |

These areas are not independent. Progress in one often depends on the others, particularly on data and AI, which underpin the rest.

Reimagining Customer Experience

Banks are rethinking how customers interact with them.

From Channels to Experiences

The shift is from managing individual channels (mobile, web, branch) to creating seamless experiences across all of them.

Example: A customer starts a mortgage application on mobile during their commute, continues desktop at work, and completes it via video call with a relationship manager, without repeating any information. The bank has a unified view of the customer and the context of their journey.

This requires unified customer data so that every touchpoint has the same information.

Personalisation at Scale

AI enables banks to move beyond generic offers to tailored, timely engagement.

Example: A bank detects that a customer’s spending has increased significantly over the past three months. Rather than waiting for the customer to request a credit limit increase, the bank proactively offers one or suggests a savings product aligned to their goals.

This level of personalisation requires real-time data and AI models that understand customer behaviour and intent.

Self-Service and Conversational AI

Chatbots and virtual assistants allow customers to resolve issues without human intervention, improving satisfaction while reducing operational costs.

Key enabler: AI models trained on the bank’s own data, with governance ensuring responses are accurate, compliant, and auditable.

Transforming Risk, Compliance, and Fraud Detection

Regulatory and risk functions are undergoing significant change.

Real-Time Fraud Detection

Traditional rule-based fraud systems are being replaced by AI-powered, real-time detection that analyses behaviour, transactions, and network patterns.

Example: Banks are using machine learning and behavioural analytics to improve fraud detection, reduce false positives, and respond faster to suspicious activity across channels.

Outcome: Faster detection, lower losses, better customer experience.

Anti-Money Laundering (AML) and Financial Crime

AI and network analysis help banks identify suspicious patterns, relationships, and behaviours that indicate money laundering or financial crime.

Regulatory context: In the UK, financial crime obligations continue to tighten, and firms are expected to strengthen controls, monitoring, and reporting. That makes better data quality, faster detection, and stronger governance increasingly important.

Regulatory Reporting and Transparency

Regulators now expect detailed, accurate reports on demand. This requires:

- Unified data across systems

- Clear data lineage and governance

- Audit trails showing how decisions and reports were generated

Banks that lack these capabilities struggle to respond quickly or confidently to regulatory inquiries.

Modernising Core Banking Systems

Many banks still run legacy core banking systems, some decades old, that are expensive, difficult to change, and incompatible with modern customer expectations.

The Challenge

- Monolithic architectures make it difficult to launch new products or integrate with third parties

- Batch processing limits real-time capabilities

- High maintenance costs consume IT budgets

The Shift

Banks are migrating to cloud-native, API-enabled core banking platforms that support:

- Real-time processing

- Modular, microservices-based architecture

- Integration with fintechs, open banking, and third-party services

Outcome: Faster innovation, lower costs, better customer experience.

Data and AI: The Foundation of Everything

Every area of transformation depends on data and AI.

Why Unified Data Platforms Matter

Most banks operate with fragmented data:

- Customer data in CRM

- Transaction data in core banking

- Risk data in compliance systems

- External data (credit bureaus, open banking) elsewhere

This fragmentation prevents banks from:

- Understanding customers holistically

- Detecting fraud across channels

- Making real-time decisions

- Scaling AI models

Unified data platforms consolidate data into a single, governed environment that enables cross-functional analytics, real-time insights, and scalable AI.

Example: A modern data platform can bring together governed data, real-time analytics, and AI capabilities in one environment, making it easier for banking teams to move from fragmented reporting to coordinated decision-making.

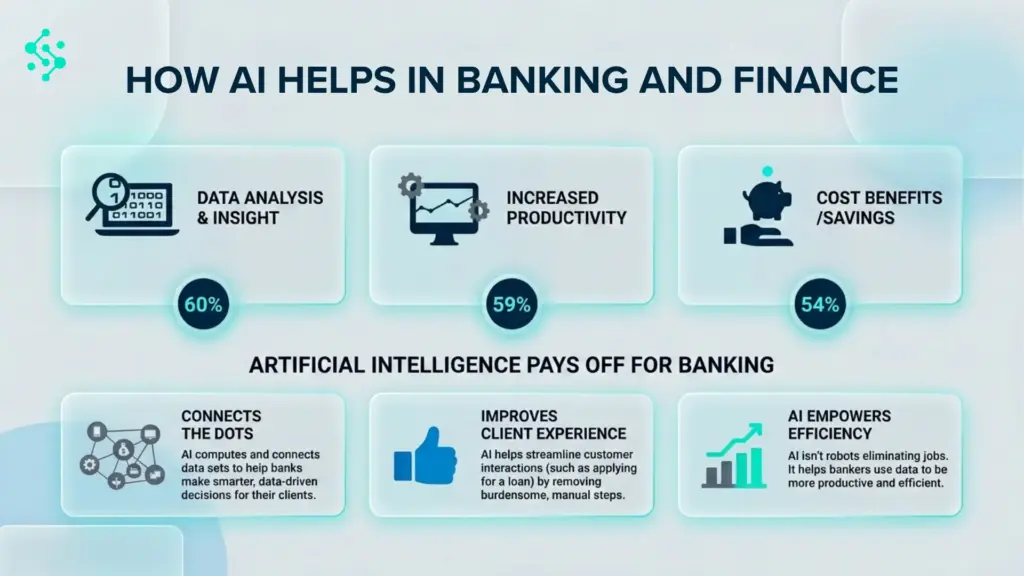

AI Use Cases in Banking

AI is now widely deployed across banking operations.

| Use Case | How AI Helps | Business Impact |

| Fraud detection | Real-time anomaly detection, behavioural analytics | Reduced fraud loss, fewer false positives |

| Credit scoring | Alternative data analysis, explainable models | Expanded lending, lower default rates |

| Customer insights | Segmentation, next-best-action, churn prediction | Improved retention, higher lifetime value |

| Regulatory compliance | Automated monitoring, suspicious activity detection | Faster reporting, reduced compliance risk |

| Conversational AI | Chatbots, virtual assistants | Improved customer experience, lower costs |

Critical requirement: AI models in banking must be explainable and auditable, particularly under GDPR and FCA expectations. Governance and transparency are not optional.

Common Challenges Banks Face

Despite clear benefits, banks face predictable obstacles.

Legacy Systems

Core banking platforms built decades ago are expensive to replace and risky to migrate. Many banks run parallel systems during transition, increasing complexity.

Data Silos

Customer, transaction, risk, and operational data are fragmented across systems, making unified analytics difficult.

Regulatory Complexity

Every change involving customer data or AI must be documented, tested, and auditable. This slows innovation and increases cost.

Scaling AI Beyond Pilots

Many banks successfully pilot AI models but struggle to scale them into production due to data quality issues, lack of governance, or unclear operating models.

Key insight: Transformation is as much an operating model and culture challenge as a technology one.

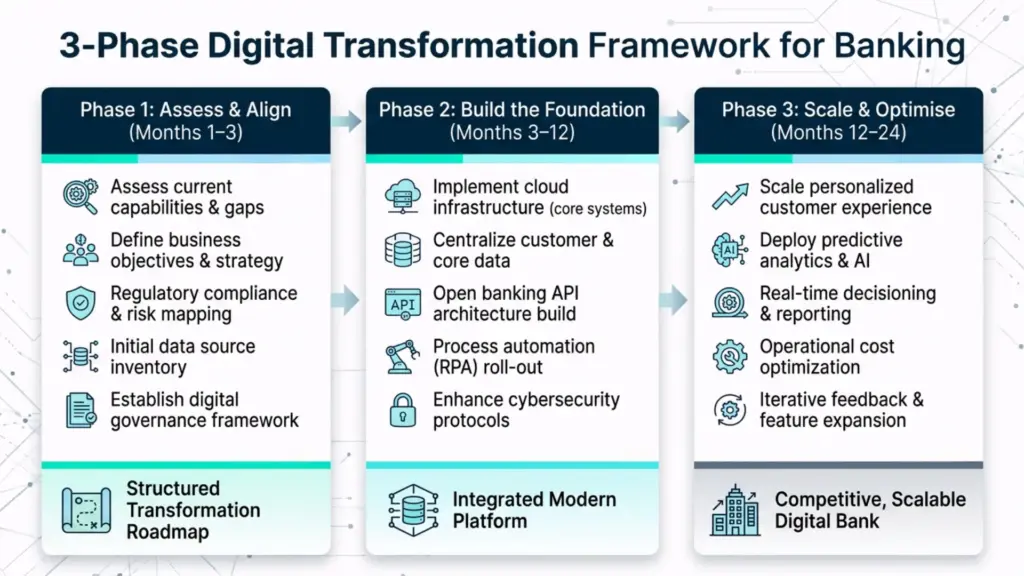

A Practical Transformation Framework

Banks that move successfully follow a phased approach.

Phase 1: Assess and Align (Months 1–3)

- Understand current state: data, systems, capabilities

- Identify priority use cases (fraud, customer experience, compliance)

- Secure executive sponsorship

- Define target operating model

Outcome: Clear roadmap with prioritised initiatives.

Phase 2: Build the Foundation (Months 3–12)

- Establish unified data platform

- Implement governance framework (data quality, access, lineage)

- Modernise core systems where critical

- Deploy 2–3 pilot use cases

Outcome: Operational data platform with proven use cases.

Phase 3: Scale and Optimise (Months 12–24)

- Scale AI models across business units

- Expand automation (compliance, customer service, operations)

- Integrate with open banking and third-party ecosystems

- Continuously improve governance and performance

Outcome: Enterprise-wide transformation delivering sustained value.

The Role of Unified Data, AI, and Governance

For banks serious about transformation, three capabilities are essential.

Unified Data Platform

Consolidates customer, transaction, risk, and external data into a single, governed environment. Enables real-time insights and scalable AI.

AI and Copilot

Powers fraud detection, credit decisions, customer insights, and automation. Copilot enables business users to query data using natural language, democratising access to insights.

Governance and Explainability

In the UK and EU, AI models must be explainable, auditable, and compliant with GDPR and FCA requirements. Banks that embed governance early scale AI faster and with less regulatory risk.

What Comes Next

Digital transformation in banking is no longer about whether to change; it is about how quickly and how well.

The banks leading in 2026 are those that have:

- Built unified data foundations

- Scaled AI across operations, risk, and customer experience

- Embedded governance from the start

- Modernised core systems to enable real-time, API-driven banking

For banks still operating with fragmented data, legacy systems, and siloed operations, the gap is widening.

The organisations that move decisively, treat transformation as data, AI, and operating model shift, not just a technology upgrade, will define the future of banking.

If your bank is working through legacy complexity, fragmented data, or pressure to scale AI responsibly, Synapx can help you turn transformation priorities into a practical roadmap, from data foundations and governance to AI use cases and operating model change.